The new year ushered in a series of warnings from the CPSC about inclined infant sleepers posing suffocation risks and dressers posing tip-over risks to consumers. Both products have been under scrutiny by the CPSC over the past year.

In October, the CPSC issued guidance urging consumers to stop using inclined infant sleep products after reports of 1,108 incidents, including 72 infant deaths. Last month, the CPSC continued to raise alarm about inclined infant sleepers by announcing the recalls of more than 165,000 sleepers from four importers due to suffocation risks. The CPSC also warned consumers about the suffocation risks posed by one brand of the inclined infant sleepers. The CPSC urged consumers to stop using the brand’s sleepers immediately.

Furniture tip-overs associated with chests and drawers have been a recent focus of the CPSC. For example, the CPSC in November announced that there were 459 reported tip-over-related deaths involving children 17 years old and younger between 2000 and 2008. This month, the CPSC warned consumers about four-drawer dressers after the manufacturer refused to issue a recall. The CPSC tested the dresser and found it was unstable and prone to tip over. The CPSC also expressed its intent to continue pressing the manufacturer to recall the dressers.

Off-highway vehicles (OHVs), which include all-terrain vehicles and utility task vehicles, also came into focus after three recalls this month due to collision hazards. Relatedly, the Consumer Federation of America issued an analysis of OHV recalls announced by the CPSC over the last decade. The analysis states that there have been 110 OHV recalls with the highest number occurring in the past three years. Most of the recalls were driven by fire (45%), throttle (14%), and steering (10%) hazards. Further, 19 brands were involved in the recalls of almost 1.5 million OHVs that resulted in at least 70 injuries and 2 deaths.

Lawyers from Hunton Andrews Kurth LLP’s insurance coverage practice provide updates on several recent recall insurance disputes:

An insurer providing contaminated products insurance to an international food distributor has filed a declaratory judgment lawsuit in New York state court seeking to bar coverage for a claim arising from a recall of defective cookie butter jars. In Berkley Assurance Company v. Acme Food Sales, Inc., Berkley alleges that a contaminated products insurance policy purchased by food importer, distributor and marketer Acme Food Sales provides no coverage for losses Acme incurred in recalling the defective cookie butter jars. The dispute began when one of Acme’s customers informed Acme that it had discovered certain jars of cookie butter contained defective inner foil seals. Acme notified its supplier of the inner seal issue and was able to trace the affected products to two lots that had been shipped to the customer. Berkley alleges, however, that the manufacturer told Acme that the defect did not present a foods safety hazard.

Berkley also alleges that the cookie butter products were not contaminated; the use of the products did not result in any bodily injury, property damage or adverse publicity; the jars were withdrawn from store shelves less than a week after Acme became aware of the issue. As a result, Berkley argues that Acme failed to satisfy any of the three requirements to trigger the policy’s accidental contamination coverage where: (i) there was no inadvertent or unintentional contamination of the products; (ii) even if there was contamination, there is no evidence that it was during or as a direct result of the products’ manufacturing, packaging or distribution; and (iii) the products did not result and would not result in any bodily injury, property damage or adverse publicity.

Berkley also asserts that the policy’s government recall coverage does not apply because neither Acme, its supplier, nor the customer had notified or communicated with a government food safety regulatory agency about the affected products. And even if they had been in touch with a government agency about the recall, Berkley states it was not advised that the recall of the cookie butter arose directly from an agency’s determination that the consumption of the products posed an unreasonable risk of serious injury or death, which is required to trigger coverage. Acme’s “voluntary” recall, Berkley argues, precludes coverage under the policy.

We will continue to monitor this dispute for further updates, including Acme’s response to Berkley’s coverage arguments.

The parties in the Kormondy product recall coverage dispute, previously reported on this blog, have reached a settlement, and the pending litigation will be dismissed within the next 30 days. Beef and poultry cooking facility Kormondy Enterprises (formerly National Steak Processors, Inc.) had sued its excess insurer in Oklahoma federal district court for denying its insurance claim arising from several lawsuits relating to a product recall of ready-to-eat chicken products.

The insurer, Great American, filed a motion for summary judgment arguing that the excess policy’s “organic pathogens” endorsement excluded coverage because the recalls were initiated because of possible undercooking and bacterial pathogens. Great American also argued that coverage for the product recalls and resulting state court litigation was excluded under various “business risk” exclusions, including an exclusion for property damage arising out of the insured’s “product,” an exclusion for “impaired property,” and a “recalled product” or “sistership” exclusion, all of which the insurer argued barred coverage for the undercooked, adulterated chicken products. Finally, even if the exclusions did not apply, Great American asserted that the policy did not provide coverage for the underlying breach of warranty claims and was never triggered because Kormondy’s primary insurance has not yet been exhausted.

Shortly after the summary judgment motion was filed, the court entered an order stating that the parties reached a settlement and that the dismissal documents would be filed by March 11, 2020. The Kormondy dispute highlights a number of common exclusions in general liability and excess policies related to products and pathogens that insurers often rely on to deny coverage for any recall-related claims. But as the coverage lawsuit and subsequent settlement show, policyholders frequently have numerous arguments for coverage that can result in recovery for defense and indemnity losses under traditional policies.

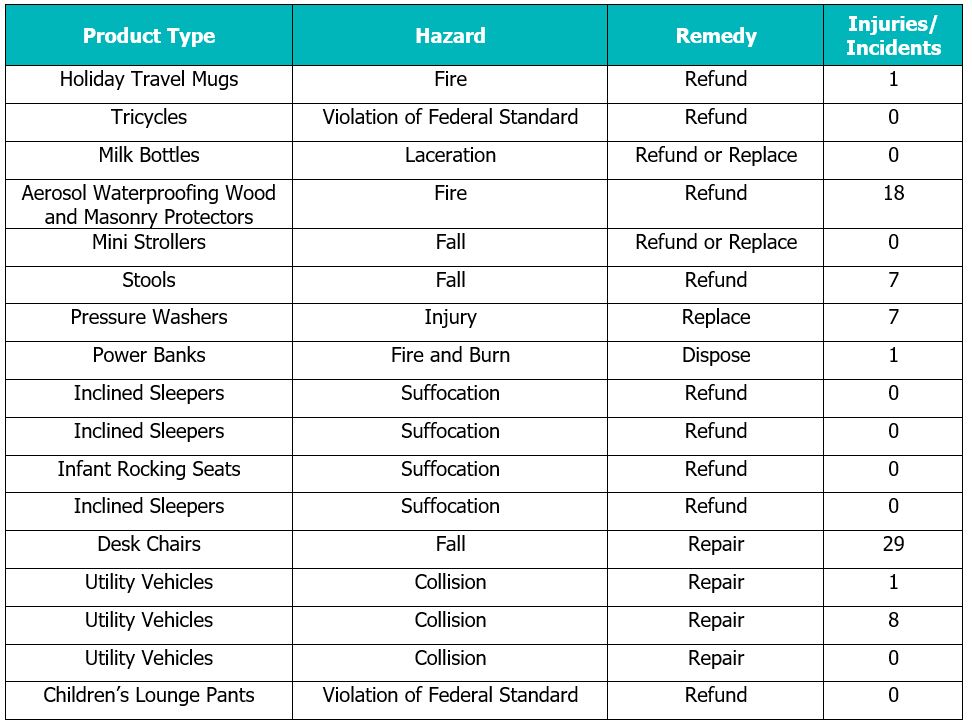

Total Recalls: 17

Hazards: Suffocation (4); Fall (3); Collision (3); Fire/Burn/Shock (3); Violation of Federal Standard (2); Laceration (1); Injury (1)

Partner

PartnerSyed represents clients in connection with insurance coverage, reinsurance matters and other business litigation. Syed serves as the head of the firm’s insurance coverage practice. He has been admitted to the US Court of Appeals ...

Partner

PartnerKelly practices as a commercial and regulatory litigator on products liability and post M&A disputes and issues and serves as one of the firm’s Deputy General Counsel focusing on law firm ethics, conflicts, and risk management ...

Partner

PartnerGeoff works closely with corporate policyholders and their directors and officers to resolve high-stakes insurance disputes. He leads the Firm’s D&O insurance and executive protection practice.

As a partner in Hunton’s ...

Search

Recent Posts

Categories

- Advertising & Marketing

- Bankruptcy

- Class Action

- Competition/Antitrust

- Consumer Protection

- Corporate Governance

- Environmental

- General

- Health Care

- Insurance

- IP

- Labor and Employment

- Mergers & Acquisitions

- Patent Infringement

- Patents

- Privacy & Cybersecurity

- Product Liability

- Real Estate

- Regulatory

- Regulatory

- Technology & E-Commerce

Tags

- 29 C.F.R. § 785.48

- 396-r

- 3D Printer

- 3D Printing

- A. Todd Brown

- A.S. Research (ASR)

- Aaron P. Simpson

- Advertisers

- Advertising

- Advertising Claims

- Advertising Idea

- Agency Guidance

- AI

- AI Interviewing Platforms

- Algorithmic Accountability Act

- Align

- Americans with Disabilities Act

- Americans with Disabilities Act (ADA)

- Andrea DeField

- Ann Marie Buerkle

- Annual Reports

- anti-aging

- Anti-Discrimination

- APEX Agreement

- Arbitration

- Arbitration Agreements

- Arizona

- Arkansas

- Arthritis

- Artificial Intelligence

- Artificial Intelligence (AI)

- Asbestos

- Assembly Bill 51 (AB 51)

- ATDS

- Australia

- Auto-renewals

- automatic telephone dialing system (ATDS)

- Automobile

- Automotive Body Parts Association (ABPA)

- Back to Work Emergency Ordinance

- biased endorsements

- Biden Administration

- Biometric Data

- Biometric Information

- Biometric Information Privacy Act (BIPA)

- BIPA

- Bitcoin

- Blockchain

- Board Diversity Disclosure

- Boards of Directors

- Bonuses

- Braille

- Branding

- Breach

- Breach of Contract

- Business Interruption Loss

- Businessowner’s Insurance

- California

- California Assembly Bill 2011

- California Employment Laws

- California Fair Employment and Housing Act

- California False Claims Act

- California Labor Code

- California Senate Bill 6

- California’s Unfair Competition Law

- CAMS

- Canada

- Cannabis

- CBD

- CBP

- CCPA

- Celebrity Endorsers

- Center for Disease Control (CDC)

- CFIUS

- CGL

- Chatbot

- Children’s Advertising

- Children’s Advertising Review Unit

- Children’s Online Privacy Protection Act (COPPA)

- China

- Christopher J. Dufek

- Christopher W. Hasbrouck

- Christy Kiely

- Class Action

- Class Actions

- Clawback

- Click-to-Cancel

- Climate Change

- clinical trials

- Collective Action

- Colorado

- Commercial General Liability

- Commercial Leasing

- Commodity Futures Trading Commission

- Compliance

- Congress

- Connecticut

- Consent

- Consent Order

- Consumer Data

- Consumer Financial Protection Bureau

- Consumer Fraud

- consumer loyalty program

- Consumer Product Safety Act

- Consumer Products

- Consumer Products Safety Commission (CPSC)

- Consumer Protection

- Consumer Review Fairness Act of 2016 (CRFA)

- Consumer Reviews

- Contamination

- Contract Law

- Controlled Substance Act

- Cookware

- COPPA

- Copyright

- Coronavirus/COVID-19

- Corp Fin

- Corporate Governance

- Corporate Reporting

- Corporate Sustainability

- Counterfeit Goods

- Counterfeit Goods Seizure Act of 2019

- CPRA

- CPSA

- CPSC

- Crack House Statute

- CRFA

- Cryptocurrency

- CSPA

- Cuba

- Currency

- Customs and Border Protection

- Cyber Coverage

- D&O

- D&O policies

- D. Andrew Quigley

- Damages

- Data Breach

- Davidson

- Deceptive Advertising

- DEI

- Delaware

- DEP

- Department of Justice

- Department of Labor

- Development Impact Fee

- Digital Assets

- digital currency

- Disclosures

- Distribution

- Division of Corporation Finance

- Dodd-Frank

- DOJ

- DOL

- Duty to Defend

- Duty to Indemnify

- e-liquid products

- Eddie Bauer

- EEOC

- Electric Vehicles

- Eleventh Circuit

- Emily Burkhardt Vicente

- Employee Rights

- Endorsement

- Endorsement Guides

- Endorsement Notice

- Endorsements

- endorser monitoring requirements

- Enforcement

- Environmental Protection Agency

- Environmental Protection Agency (EPA)

- EPA

- Epidemic

- ESG

- ESG Disclosure

- EU Regulation

- European Union

- European Unitary Patent

- EV Charging

- Exceptions

- Exclusions

- Exercise Machines

- Extended Producer Responsibility (EPR)

- FAA

- Fair Labor Standards Act

- Fair Labor Standards Act (FLSA)

- fair use

- False Advertising

- False Advertising Claims

- False Advertising Law

- False Claims Act

- Family Leave Policies

- FCC

- FCRA

- FDA

- Federal Arbitration Act (FAA)

- Federal Communications Commission

- Federal District Court

- Federal Trade Commission

- Federal Trade Commission (FTC)

- FFDCA

- FIFRA

- Fifth Circuit

- Final Rule

- Fireworks

- First Amendment

- Fixing America’s Surface Transportation (FAST) Act

- Florida

- Florida House of Representatives (HB 963) and Florida Senate (SB 1670)

- Florida Legislature

- FLSA

- FLSA/Wage & Hour

- food delivery

- Food Safety

- Form 10-K

- Formaldehyde Standards for Composite Wood Products Act of 2010

- fractional interests

- Franchise

- Frederic Chang

- Free Trials

- FTC

- FTC Act

- Gavin Newsom

- GDPR

- General Liability

- Geoffrey B. Fehling

- Georgia

- Gift Cards

- GoodRx

- Gramm-Leach-Bliley (GLB) Act

- Green

- Green Guides

- Greenhouse Gas

- Gun Safety

- Hart-Scott-Rodino

- Hart-Scott-Rodino (HSR)

- hashtag

- Hawaii

- Health Care

- Health Claims

- Hedge Fund

- HIPAA

- hoverboards

- human capital

- Human Rights

- Illinois

- Illinois Artificial Intelligence Video Interview Act (the Illinois Act)

- Illinois Biometric Information Privacy Act (BIPA)

- Indiana

- Influencer Marketing

- Infringement

- initial public offerings (IPOs)

- Injury

- Insurance

- Insurance Loss

- Insurance Provider

- Intellectual Property

- Intellectual Property Licenses in Bankruptcy Act

- Interest Rate

- International

- International Trade Commission

- International Trade Commission (ITC)

- INVISALIGN

- Iowa

- IP

- Ireland

- IT

- ITC

- iTERO

- Junk Fees

- Katherine Miller

- Kurt A. Powell

- Kurt G. Larkin

- Labeling Rules

- Labor

- Labor Code Private Attorneys General Act of 2004 (PAGA)

- Labor Organizing

- Labor Unions

- Land Use

- Landlord

- Latin America

- Lautenberg Act

- Lawsuit Reform Alliance of New York (LRANY)

- Lead

- Lease

- Legislation

- Leveraged Loans

- Liability Insurance Policy

- Liberty Insurance Corporation

- Liberty Mutual Fire Insurance Company

- LIBOR Discontinuation

- liquidity

- Litigation

- Live Chat

- Louisiana

- M&A

- Made in the USA

- Made in USA

- MagicSleeve

- Magnuson-Moss Warranty Act

- Magnuson-Moss Warranty Act (MMWA)

- Maine

- Malcolm C. Weiss

- Manufacturing

- Marketing Claims

- Maryland

- Massachusetts

- Matthew T. McLellan

- Maya M. Eckstein

- MD&A

- Medtail

- Membership cancellation

- Metaverse

- MeToo Movement

- Mexico

- Michael J. Mueller

- Michael S. Levine

- Minimum Wage

- Minnesota

- Minnesota Pollution Control Agency (MPCA)

- Misclassification

- Mislabeling

- Mission Product Holdings

- Missouri

- Mobile

- Mobile App

- Multi-Level Marketing Program (MLM)

- NAA

- NAD

- NASA

- National Advertising Division

- National Advertising Division (NAD)

- National Advertising Review Board

- National Products Inc.

- National Retail Federation

- Natural Disaster

- Nebraska

- Neil K. Gilman

- Network Outage

- Nevada

- New Jersey

- New York

- NHTSA

- NIL rights

- Ninth Circuit

- NLRA

- NLRB

- no-action request

- non-fungible token (NFT)

- North Carolina

- Obama Administration

- Occupational Safety and Health Administration (OSHA)

- Occurrence

- Office of Labor Standards Enforcement

- Ohio

- Oklahoma

- Online Cash Providers

- Online Retailer

- online reviews

- Opioids

- Oregon

- Overboarding

- Overtime

- Overtime Exemptions

- Ownership

- Packaging

- PAGA

- Pandemic

- Patent

- Patent Infringement

- Patents

- Paul T. Moura

- Pay Ratio

- pay-to-play rankings

- Penalty

- Pennsylvania

- Personal and Advertising Injury

- Personal Data

- Personal Information

- Personally Identifiable Information

- Pesticides

- PFAS

- Physical Loss or Damage

- Policy

- price gouging

- Privacy

- Privacy Guidelines

- Privacy Policy

- Privacy Protections

- Prohibition on Sale

- Property Insurance

- Property Rights

- Proposition 65

- Proxy Access

- proxy materials

- Proxy Statements

- Public Companies

- Purdue Pharma

- Randall S. Parks

- Ransomware

- real estate

- Recall

- Recalls

- Regulation

- Regulation S-K

- Restaurants

- Restrictive Covenants

- Retail

- Retail Development

- Retail Industry Leaders Association

- Retail Litigation Center

- Rounding

- Rulemaking

- Ryan A. Glasgow

- Sales Tax

- Scott H. Kimpel

- SD8 coins

- SEC

- SEC Disclosure

- Second Circuit

- Section 337

- Section 365

- Secure and Fair Enforcement Banking Act of 2019 (“SAFE Banking Act”)

- Securities

- Securities and Exchange Commission

- Securities and Exchange Commission (SEC)

- security checks

- Senate

- Senate Data Handling Report

- Sergio F. Oehninger

- Service Contract Act (SCA)

- Service Provider

- SHARE

- Shareholder

- Shareholder Proposals

- Slogan

- Smart Contracts

- Social Media

- Social Media Influencers

- Software

- South Carolina

- South Dakota

- Special purpose acquisition companies (SPACs)

- State Attorneys General

- Store Closures

- Subscription Services

- Substantiation

- Substantiation Notice

- Supplier

- Supply Chain

- Supply contracts

- Supreme Court

- Sustainability

- Syed S. Ahmad

- Synovia

- Targeted Advertising

- Tax

- TCCWNA

- TCPA

- Technology

- Telemarketing

- Telephone Consumer Protection Act

- Telephone Consumer Protection Act (TCPA)

- Tempnology LLC

- Tenant

- Tennessee

- Terms and Conditions

- Texas

- the Fair Credit Reporting Act (FCRA)

- Thomas R. Waskom

- Title VII

- tokenization

- tokens

- Toxic Chemicals

- Toxic Substances Control Act

- Toxic Substances Control Act (TSCA)

- Trade Dress

- Trademark

- Trademark Infringement

- Trademark Trial and Appeal Board (TTAB)

- TransUnion

- Travel

- Trump Administration

- TSCA

- TSCA Title VI

- U.S. Department of Justice

- U.S. Department of Labor

- U.S. Food and Drug Administration

- U.S. House of Representatives

- U.S. Patent and Trademark Office

- Umbrella Liability

- Union

- Union Organizing

- United Specialty Insurance Company

- Unmanned Aircraft

- Unruh Civil Rights Act

- UPSTO

- US Chamber of Commerce

- US Customs and Border Protection (CBP)

- US Environmental Protection Agency (EPA)

- US International Trade Commission (ITC)

- US Origin Claims

- US Patent and Trademark Office

- US Patent and Trademark Office (USPTO)

- US Supreme Court

- USDA

- USPTO

- Utah

- Varidesk

- Vermont

- Virginia

- volatile organic compound (VOC) emissions

- W. Jeffery Edwards

- Wage and Hour

- Walter J. Andrews

- Warranties

- Warranty

- Washington

- Washington DC

- Web Accessibility

- Weight Loss

- Wiretapping

- World Health Organization (WHO)

- Wyoming

- Year In Review

- Zoning Regulations

Authors

- Gary A. Abelev

- Alexander Abramenko

- Yaniel Abreu

- Syed S. Ahmad

- Nancy B. Beck, PhD, DABT

- Brandon Bell

- Fawaz A. Bham

- Michael J. “Jack” Bisceglia

- Jeremy S. Boczko

- Brian J. Bosworth

- Shannon S. Broome

- Samuel L. Brown

- Tyler P. Brown

- Melinda Brunger

- Jimmy Bui

- M. Brett Burns

- Olivia G. Bushman

- Matthew J. Calvert

- María Castellanos

- Grant H. Cokeley

- Abigail Contreras

- Alexandra B. Cunningham

- Merideth Snow Daly

- Javier De Luna

- Timothy G. Decker

- Andrea DeField

- John J. Delionado

- Stephen P. Demm

- Mayme Donohue

- Nicholas Drews

- Christopher J. Dufek

- Robert T. Dumbacher

- M. Kaylan Dunn

- Chloe Dupre

- Frederick R. Eames

- Maya M. Eckstein

- Tara L. Elgie

- Clare Ellis

- Latosha M. Ellis

- Juan C. Enjamio

- Kelly L. Faglioni

- Ozzie A. Farres

- Geoffrey B. Fehling

- Hannah Flint

- Erin F. Fonté

- Kevin E. Gaunt

- Andrew G. Geyer

- Armin Ghiam

- Neil K. Gilman

- Ryan A. Glasgow

- Tonya M. Gray

- Aidan Gross

- Elisabeth R. Gunther

- Steven M. Haas

- Kevin Hahm

- Jason W. Harbour

- Jeffrey L. Harvey

- Christopher W. Hasbrouck

- Eileen Henderson

- Gregory G. Hesse

- Kirk A. Hornbeck

- Rachel E. Hudgins

- Jamie Zysk Isani

- Nicole R. Johnson

- Roland M. Juarez

- Suzan Kern

- Jason J. Kim

- Scott H. Kimpel

- Andrew S. Koelz

- Leslie W. Kostyshak

- Perie Reiko Koyama

- Torsten M. Kracht

- Brad Kuntz

- Kurt G. Larkin

- Tyler S. Laughinghouse

- Matthew Z. Leopold

- Michael S. Levine

- Ashley Lewis

- Abigail M. Lyle

- Maeve Malik

- Phyllis H. Marcus

- Eric R. Markus

- Brandon Marvisi

- John Gary Maynard, III

- Aubrianna L. Mierow

- Gray Moeller

- Reilly C. Moore

- Michael D. Morfey

- Ann Marie Mortimer

- Michael J. Mueller

- J. Drei Munar

- Marcus E. Nelson

- Matthew Nigriny

- Justin F. Paget

- Christopher M. Pardo

- Randall S. Parks

- Katherine C. Pickens

- Gregory L. Porter

- Kurt A. Powell

- Robert T. Quackenboss

- D. Andrew Quigley

- Michael Reed

- Shawn Patrick Regan

- Jonathan D. Reichman

- Kelli Regan Rice

- Patrick L. Robson

- Amber M. Rogers

- Natalia San Juan

- Katherine P. Sandberg

- Arthur E. Schmalz

- Daniel G. Shanley

- Madison W. Sherrill

- Kevin V. Small

- J.R. Smith

- Bennett Sooy

- Daniel Stefany

- Katherine Tanzola

- Javaneh S. Tarter

- Jessica N. Vara

- Emily Burkhardt Vicente

- Mark R. Vowell

- Gregory R. Wall

- Thomas R. Waskom

- Malcolm C. Weiss

- Holly H. Williamson

- Samuel Wolff

- Steven L. Wood

- Jingyi “Alice” Yao

- Jessica G. Yeshman